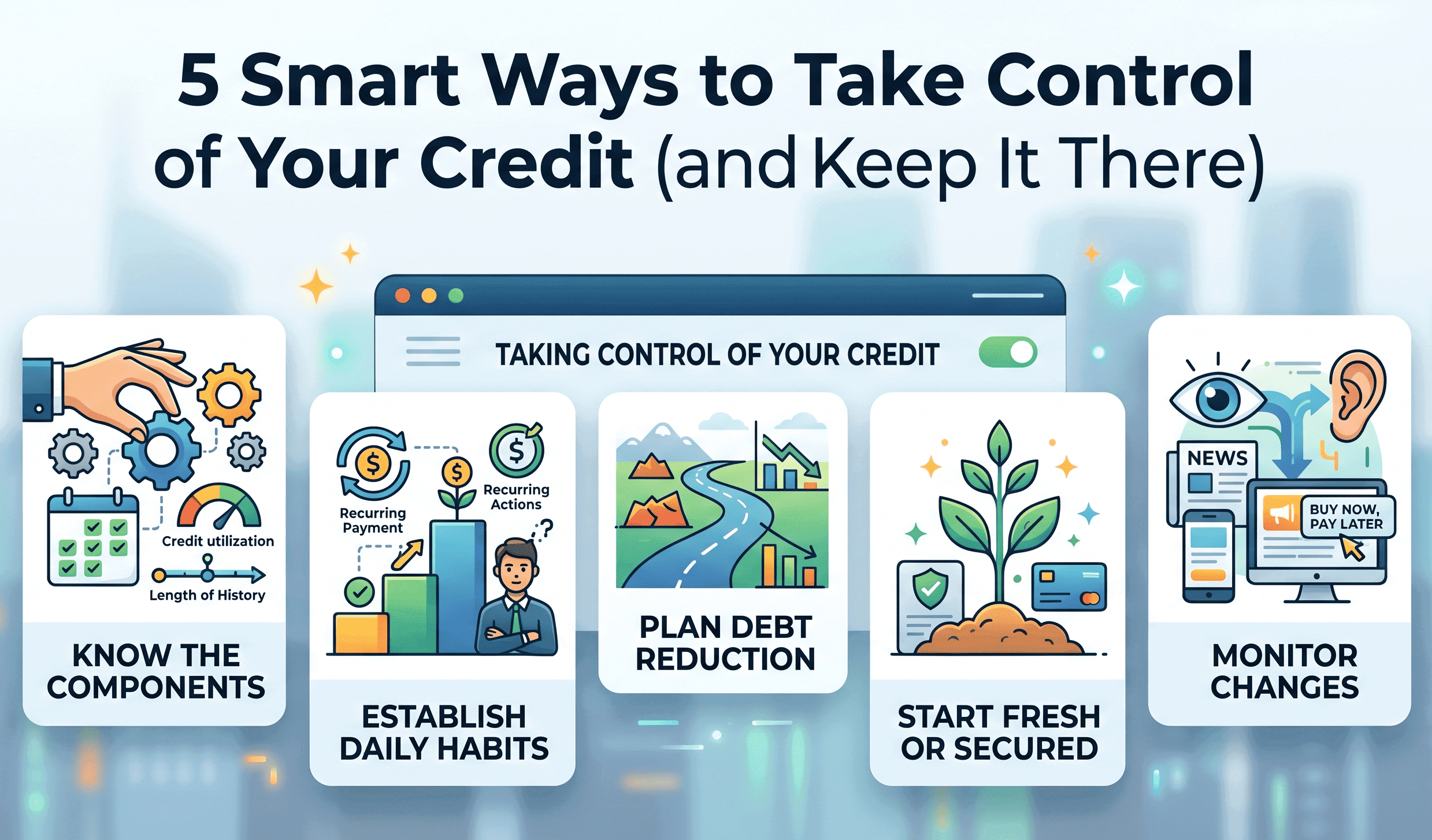

5 Smart Ways to Take Control of Your Credit (and Keep It There)

Your credit score is more than a number, it’s a tool that you’ll use throughout our day to day life for years to come. When you understand how it works, you can use it to assist you in building a strong financial future.

Here are five practical ways to manage your credit with confidence.

Understand What Builds Your Credit Score

Your credit score is built from a few core behaviors: payment history, credit utilization, length of credit history, credit mix, and new credit activity.

Payment history – This is the most important factor. Lenders want to see that you consistently pay your obligations on time. Even one missed payment can have a noticeable impact, but the good news is that consistent on-time payments over time can help rebuild your score.

Credit utilization – This measures how much of your available credit you’re using. For example, if you have a $1,000 limit and a $300 balance, you’re using 30%.

Length of credit history – The longer your accounts have been open, the more data lenders have to evaluate your habits. This is why keeping older accounts open can be beneficial, even if you don’t use them often.

Credit mix – Having a variety of credit types, such as credit cards and loans, can show that you can manage different financial responsibilities. This matters less than payment history and utilization, but it still plays a role.

New credit activity – Applying for multiple accounts in a short period can signal risk to lenders. Being intentional about when and why you apply helps protect your score.

A good credit score generally falls within the range of 670 to 850, with higher scores giving you access to better rates, terms, and financial opportunities. You can check your credit report for free through AnnualCreditReport.com, which allows you to review your information, monitor changes, and catch any errors early. And don’t worry, checking your credit report yourself won’t negatively impact your credit score.

Build Strong Credit Habits That Last

Strong credit is built from small, consistent actions that become part of your routine. These habits help you maintain stability, even when your financial situation changes. Some positive credit building habits include:

- Pay on time, every time – Even if you can only make the minimum payment, staying current protects your credit and keeps negative marks off your report.

- Keep balances low and manageable – A good rule of thumb is to stay below 30% of your credit limit, but aiming lower when possible can have an even stronger impact.

- Use credit regularly, but intentionally – Small, manageable purchases that you pay off can help demonstrate consistent activity without increasing risk.

- Keep older accounts open – Closing accounts can shorten your credit history and increase your utilization ratio, which may lower your score.

- Limit unnecessary applications – Each application can result in a hard inquiry, so spacing them out and applying with purpose helps maintain stability.

Focusing on paying on time and keeping balances low will address the most impactful parts of your credit score. Simple systems, like autopay or setting reminders, can help turn these behaviors into consistent habits. Review your balances regularly or choosing one account to focus on paying down can help you stay engaged and in control of your credit over time.

Create a Clear Plan to Manage and Reduce Debt

If you’re carrying debt, it can feel overwhelming—but having a plan can turn that stress into something you can actually work through. Debt becomes a lot more manageable when you understand it and take small, consistent steps forward.

Here’s a simple way to approach it:

- Start by getting a clear picture – Lay everything out: your balances, interest rates, and minimum payments. It might not feel great to look at all at once, but having it in front of you gives you clarity—and that’s where real progress begins.

- Choose a payoff approach that works for you – There’s no one “right” way to do this. Some people feel motivated paying off smaller balances first, while others focus on high-interest debt to save money over time. The best strategy is the one you’ll actually stick with.

- Take a step toward collections accounts – If you have accounts in collections, you’re not stuck. You can reach out to explore payment plans or possible settlements. It might feel uncomfortable at first, but even starting the conversation can help you regain a sense of control.

- Know that progress counts more than perfection – Credit scoring is evolving, and paid collections are starting to carry less weight than they used to. That means taking action—even on older debt—can help support your recovery over time.

- Keep showing up for your current accounts – As you work through past debt, continuing to make on-time payments now helps rebuild trust and strengthen your credit moving forward.

Establish Credit If You’re Just Getting Started

If you’re new to credit (or new to the U.S.) you’re starting with a blank slate. That can feel limiting at first, but it’s also a real opportunity to build strong habits from the very beginning.

Because credit history doesn’t always transfer between countries, lenders need to see new activity before they can understand how you manage money. The goal isn’t to take on a lot—it’s to show consistency over time.

Here are a few simple ways to get started:

- Use a secured credit card – This is one of the most accessible options. You make a deposit that becomes your credit limit, and as you use it and pay it off on time, you begin building your credit history.

- Become an authorized user – Joining a trusted person’s account (like a family member or partner) can help you benefit from their established history—as long as the account is in good standing.

- Try a credit-builder loan – These are designed specifically to help you build credit. You make small, consistent payments, which get reported and help create a positive track record.

- Start small and stay consistent – Use credit in simple, manageable ways, like a small purchase you can pay off easily. Paying on time is what really builds trust over time.

- Know that more data is being recognized – Newer systems are starting to include things like rent and utility payments, which can help expand access to credit for those just getting started.

Stay Informed About Changes That Affect Your Credit

Credit systems are always evolving, and staying informed helps you make confident, well-informed decisions about your finances.

Here are a couple of important updates to be aware of:

Medical debt – Newer credit scoring models are beginning to place less weight on certain medical collections, especially once they’ve been paid. In some cases, smaller medical debts may not appear on your credit report right away. This shift reflects a broader understanding that medical expenses are often unexpected and not always within your control, which means addressing them can still support your credit over time.

Buy Now, Pay Later (BNPL) – These services can make purchases feel more manageable by breaking them into smaller payments, but they still require intentional use. While many BNPL accounts aren’t consistently reported to credit bureaus today, missed payments can still lead to fees or collections—which can impact your credit. As reporting continues to evolve, these accounts may become more visible, so it’s helpful to treat them like any other financial commitment.

As reporting continues to change, treating every payment commitment as part of your overall financial picture can help you stay consistent, avoid surprises, and keep your credit moving in the right direction.