5 Things You Should Know Before Buying a Home

Buying a home is one of the most significant financial decisions you can make. For many people, it’s a major milestone that represents stability, independence, and the opportunity to build wealth over time.

Before you start browsing listings or attending open houses, it’s important to understand what homeownership involves so you can make informed decisions and prepare yourself for a successful home-buying journey.

Here are five things everyone should know before buying a home.

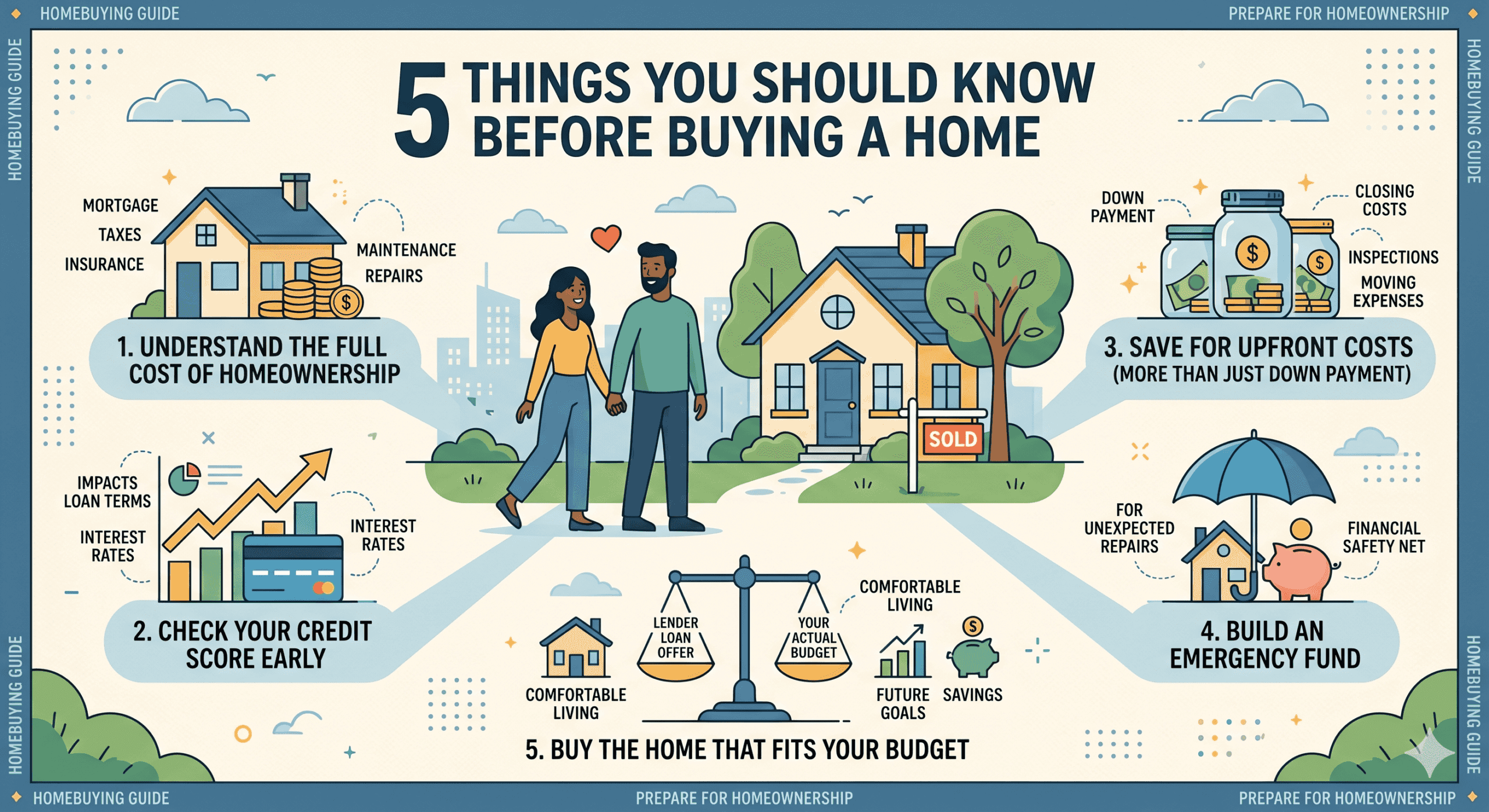

The Cost of Homeownership Goes Beyond the Mortgage

When people think about buying a home, they often focus on the monthly mortgage payment. While your mortgage will likely be your largest housing expense, it’s only one part of the overall cost of owning a home.

As a homeowner, you may also be responsible for property taxes, homeowners insurance, utilities, maintenance, repairs, and, in some cases, homeowners association (HOA) fees. Unlike renting, there isn’t a landlord to call when something breaks. If the water heater stops working or the roof needs repairs, those costs typically fall on you.

Before buying a home, take time to understand the full costs of ownership in your area. Looking at the complete financial picture can help you avoid surprises and determine what you can comfortably afford.

Your Credit Score Can Impact Your Buying Power

Your credit score is one of the most important factors lenders consider when reviewing your mortgage application. It helps lenders evaluate your creditworthiness and can influence whether you’re approved for a loan, how much you can borrow, and the interest rate you receive.

A stronger credit score can often lead to better loan terms, which may save you thousands of dollars over the life of your mortgage. Simple habits like paying bills on time, reducing outstanding debt, and regularly monitoring your credit report can help strengthen your financial profile over time. Even small improvements can make a meaningful difference when you’re ready to apply for a mortgage.

That’s why it’s a good idea to review your credit well before you begin the home-buying process.

Save for More Than Just The Down Payment

Many prospective homebuyers spend years saving for a down payment, and for good reason, homes aren’t cheap! However, the down payment is only one of several upfront costs you’ll likely encounter.

Depending on your situation, you may also need funds for closing costs, home inspections, appraisals, moving expenses, and immediate repairs or upgrades after moving in. That’s why it’s important to build a savings plan that accounts for more than just your down payment goal.

It’s a good idea to aim to save at least 3%–5% of your home’s expected purchase price in addition to your down payment. While every home purchase is different, having extra savings set aside can help with unexpected costs that often arise during the home-buying process.

The more prepared you are before purchasing a home, the more flexibility you’ll have throughout the process.

Build An Emergency Fund

Once you’ve planned for your down payment and upfront home-buying expenses, consider maintaining a separate emergency fund. Many financial experts recommend keeping three to six months of essential expenses in savings, which can help you manage unexpected home repairs or other financial surprises after you move in without relying on credit cards or disrupting your other financial goals.

Whether it’s a plumbing issue, a broken appliance, or routine maintenance that costs more than expected, an emergency fund can provide peace of mind and help you navigate homeownership with preparedness.

Buy the Home That Fits Your Budget, Not Just the One You Qualify For

One of the most important lessons for prospective homeowners is that affordability and loan approval are not always the same thing.

A lender may approve you for a certain loan amount, but that doesn’t necessarily mean borrowing the maximum amount is the best choice for your financial future.

A home should support your goals without stretching your budget so thin that you struggle to save, invest, pay down debt, or enjoy life’s other priorities.

When considering how much home you can afford, ask yourself:

- Is there still room to build savings?

- Will I be able to financially prepare for emergencies?

- Can I still contribute to retirement?

- Will I be able to pursue the financial goals that matter most to me?