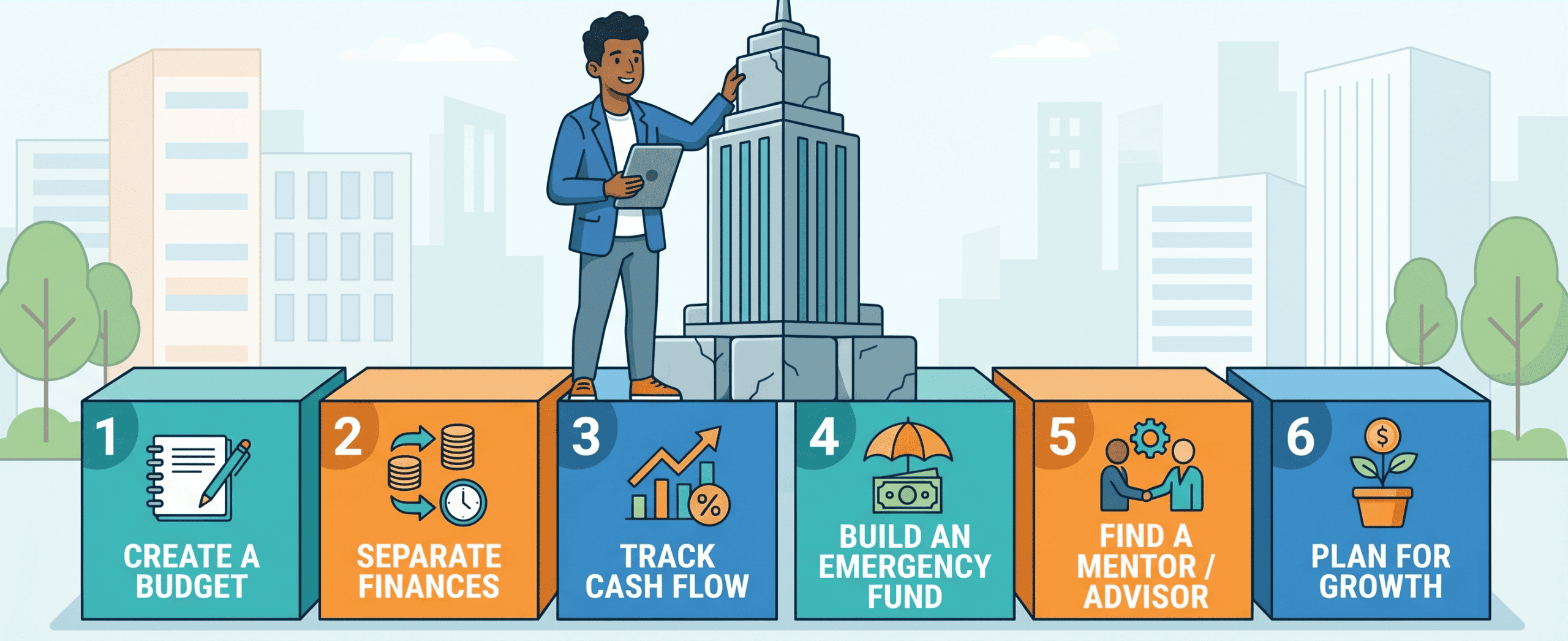

Six Lessons for Building Your Business: The Financial Foundations Every Entrepreneur Needs

Starting a business can be one of the most empowering decisions you can make, and one of the most humbling. The good news? You don’t have to learn everything the hard way. Here are six foundational lessons on entrepreneurship and financial literacy that will help you move forward with confidence and clarity.

Draw a Hard Line Between Business and Personal Money

One of the most common and costly mistakes new entrepreneurs make is blending their personal finances with their business finances. It may feel harmless at first, but it can quietly cause you to lose visibility into whether your business is actually healthy and drain the capital that could be working for your growth.

Think of it this way: even if you’re the founder, owner, and CEO, pay yourself like an employee. Set a defined personal draw and keep the rest in the business. This discipline allows you to reinvest, hire, and scale. The sooner you treat yourself as an employee of your own business, the sooner you’ll have the capital to actually grow it.

This also means opening separate bank accounts — one for your business, one for personal use. It’s a simple move that will help to remove confusion down the road.

YOUR NEXT STEP

Open a dedicated business checking account this week if you haven’t already. Even if you’re freelancing or just getting started, separating your income is one of the most important financial habits you can build.

Plan for Taxes Before the Bill Arrives

Something that is often overlooked when embarking on the entrepreneurial journey is taxes. When you’re a W2 employee, your employer handles it automatically. The moment you’re self-employed or running a business, that responsibility falls on you. If you’re not prepared, a large tax bill can appear seemingly out of nowhere.

The rule of thumb that has helped countless entrepreneurs: the moment any payment lands in your account, move 20% of it into a separate savings account where you won’t be tempted to touch it.

Beyond the basics, tax planning (not just tax paying) is where real financial leverage happens. A good accountant or financial advisor who understands business can help you keep more of what you earn through smart structuring, deductions, and retirement strategies.

YOUR NEXT STEP

Set up automatic transfers so that 20–25% of each deposit moves to a dedicated tax-savings account.

Build a Cash Cushion Before You Need One

Business isn’t a straight line. There are slow seasons, lost clients, unexpected costs, and events that no one sees coming. The businesses that survive difficult moments are the ones that prepare for them in advance.

A practical way to plan for difficult times is to work towards keeping 10% of your annual revenue in a business savings account as operating capital. For instance, if you’re generating $100,000 in revenue, $10,000 is in reserve. It may not be glamorous, but having a buffer will give you options when the unexpected happens.

Also, keep in mind that strategic business debt is not an enemy. Building a banking relationship and establishing a line of credit can be a flexible tool for things like bridging slow months, funding growth, or covering a hiring decision. Just remember that a credit line is an operational tool, not a lifestyle upgrade, so it’s still important to be mindful of your spending decisions.

YOUR NEXT STEP

Look at your current revenue and calculate what 10% would look like as a savings target. If you’re not at a place to save 10%, try setting aside 2–3%. The percentage can grow as your business grows.

Embrace the Season of Sacrifice — It Has an End Date

Entrepreneurship is often talked about in terms of freedom and flexibility, and it absolutely can be. But in the early years, it may look more like long workdays, delayed gratification, and making peace with uncertainty.

But keep in mind, the sacrifice is finite. It is a season, not a sentence. The people who build lasting businesses are willing to make difficult personal sacrifices because they understand that what they’re building is something no W2 job could ever provide.

Ask yourself honestly: what am I willing to sacrifice to build my business? Be as honest as you can with yourself about the answer. The decision is completely yours.

YOUR NEXT STEP

Write down what your non-negotiables are. Knowing your boundaries helps you make smarter decisions in difficult times.

Protect Your Time Like It’s Your Most Valuable Asset — Because It Is

Early-stage entrepreneurs wear every hat. You’re the salesperson, the scheduler, the customer service rep, and the janitor, sometimes all in the same afternoon. That’s normal, and there’s real value in understanding every part of your business from the ground up. However, spending your valuable hours on low-value tasks will inevitably keep you from doing the high-value work that actually grows your business.

To see where you’re spending the most time, jot down everything you do in a given week. Then identify two categories: the things you genuinely enjoy and the things that directly drive revenue. Start planning to delegate, subcontract, or systematize it as soon as you’re able.

This isn’t just about efficiency, it’s about building a business that can grow beyond you. Protecting your time for your highest-value work is how you prevent that ceiling from closing in.

YOUR NEXT STEP

Do a “time audit” this week. List every task you handle. Highlight the ones that only you can do. Circle the ones you could hand off. That list is your delegation roadmap.

Share Your Vision — You Can’t Build in Silence

Many first-time entrepreneurs hold their ideas close, afraid someone will steal the concept, or that sharing too early invites judgment. But here’s what experienced entrepreneurs know: capital follows conviction. If you can clearly articulate what you’re building and why, you’ll be surprised who may show up to help.

Don’t be afraid to share your idea so that the people who could help you can. Seek out people who are just a few years ahead of you on the path as mentors. Their perspective is most relevant, more accessible, and highly actionable. When you’re further along, pay it forward in the same way.

YOUR NEXT STEP

Identify one person in your network who is 2–3 years ahead of you in business. Reach out this week and ask three specific questions. Then identify one person behind you that you could do the same for.